The Week in Charts

Market Recap

Stocks Tumble as Economic Concerns Mount

The U.S. stock market experienced a significant downturn in the week ending September 6th, with major indices recording their worst performance in over a year. The S&P 500 fell more than 4%, marking its steepest weekly decline since early 2023. Smaller companies and technology stocks bore the brunt of the sell-off, with the Russell 2000 and NASDAQ dropping 6.2% and 5.8%, respectively.

Several factors contributed to the market’s poor performance. Investors grew increasingly worried about the Federal Reserve’s monetary policy, fearing that potential interest rate cuts might come too late to prevent an economic slowdown. This concern was exacerbated by disappointing economic data, particularly in the labor and manufacturing sectors.

Sector Performance and Notable Movements

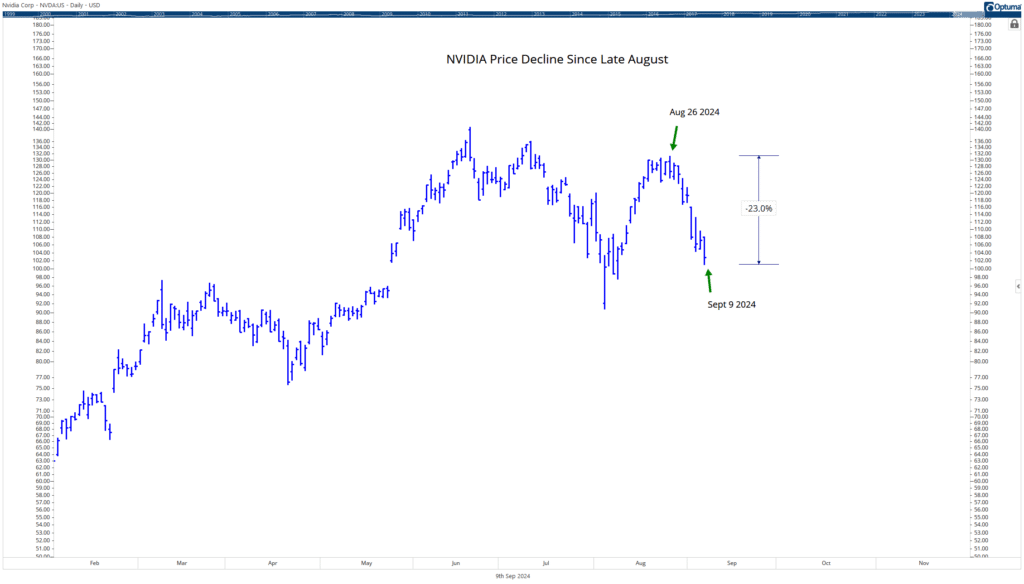

The Information Technology sector was hit hardest, declining 7% over the week. Nvidia, a major player in the semiconductor industry, saw its stock price plummet by approximately 14% amid rumors of a potential antitrust investigation by the Justice Department.

In contrast, traditionally defensive sectors such as Consumer Staples, Real Estate, and Utilities showed relative resilience during the market downturn.

Labor Market Softens

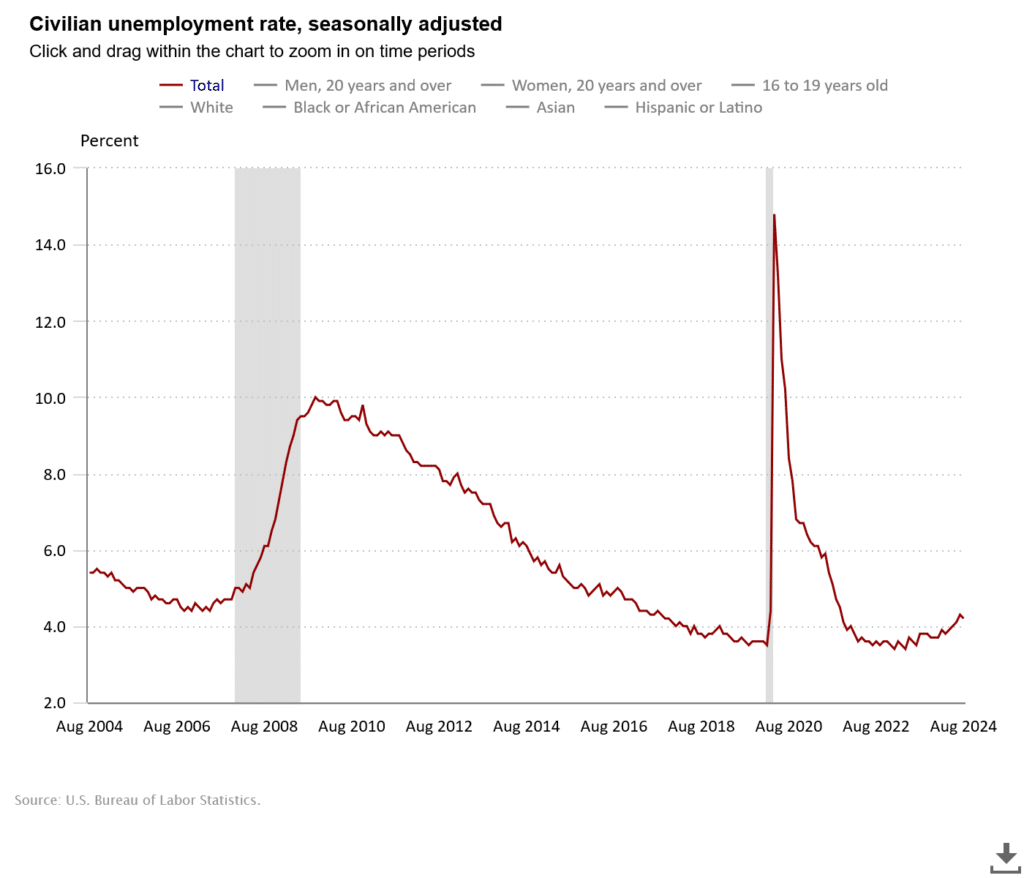

The latest employment report from the U.S. Bureau of Labor Statistics revealed a softer job market than anticipated. August saw the addition of 142,000 nonfarm payroll jobs, falling short of economists’ expectations.

The unemployment rate edged down slightly to 4.2%, but remains higher than the 3.8% recorded a year ago. The number of unemployed individuals now stands at 7.1 million, up from 6.3 million in the previous year.

Some positive news emerged from the report, with a decrease of 190,000 in the number of people on temporary layoff. However, the long-term unemployment situation remained largely unchanged, with 1.5 million individuals jobless for 27 weeks or more, accounting for 21.3% of all unemployed people.

Manufacturing Sector Continues to Struggle

The Institute for Supply Management’s Manufacturing PMI, a key indicator of factory activity, showed that the manufacturing sector contracted for the fifth consecutive month in August.

The index registered 47.2%, a slight improvement from July’s 46.8%, but still below the 50% threshold that separates expansion from contraction.

Only one of the five subindexes contributing to the Manufacturing PMI showed expansion, highlighting the ongoing challenges faced by this sector.

Commodity Price Fluctuations

The ISM report also provided insights into commodity price trends. Several items, including aluminum, corrugate, electrical components, and plastic resins, saw price increases.

Conversely, commodities such as copper, natural gas, and various steel products experienced price declines. The report also noted ongoing supply shortages in electrical and electronic components, as well as hydraulic components and pigments.

Looking Ahead

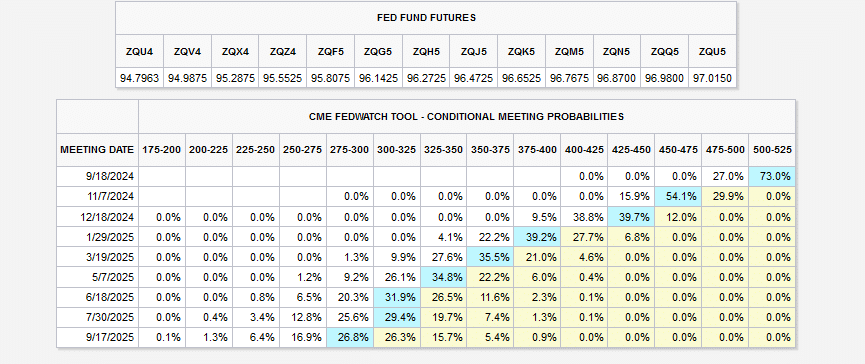

source: CME Group

As the Federal Reserve’s next policy meeting approaches in less than two weeks, market participants are closely watching economic indicators for clues about future monetary policy decisions. While a rate cut is widely anticipated, the probability of a larger 50 basis point reduction has decreased to around 30%.

The combination of weaker-than-expected job growth, persistent manufacturing contraction, and volatile commodity prices has created a complex economic landscape. Investors and policymakers alike will be keenly observing upcoming data releases to gauge the overall health of the U.S. economy and determine the most appropriate course of action to support sustainable growth while managing inflationary pressures.

What’s Going On In Your Portfolio?

Client portfolios are partially invested at this time, favoring value names over their growth counterparts. Historically, markets have been weak as we get closer to the Presidential election. During this time, we will be watching for opportunities at lower prices.

Client portfolios are partially invested at this time, favoring value names over their growth counterparts. Historically, markets have been weak as we get closer to the Presidential election. During this time, we will be watching for opportunities at lower prices.

Bond portfolios continue to be fully invested in High Yield bonds, which is an indication that the longer term trend of the market is still intact.

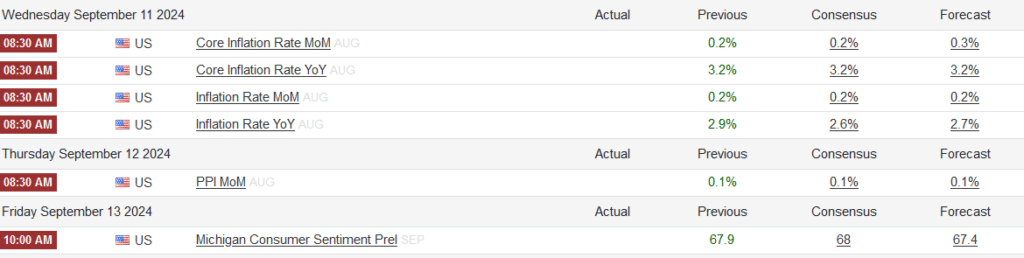

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics