Market Recap

The U.S. equity markets displayed mixed results this week, with a notable shift from last week’s trends:

- The Russell 2000, representing smaller-cap stocks, was the only major index to decline, pushing it back into negative territory for the year-to-date.

- The S&P 500 Index continued its upward trajectory, reaching new record highs.

- Growth stocks significantly outperformed value stocks.

- The NASDAQ maintained its impressive momentum, surging 3.5% for the week. This represents a remarkable recovery of over 70% from its late 2022 lows.

Trading was subdued due to the Independence Day holiday on Thursday and typical seasonal patterns, resulting in light trading volumes.

Economic Data and Fed Expectations

A wealth of economic data was released this week, covering various sectors:

- Manufacturing

- Jobless claims

- Construction spending

Most of these reports were interpreted as “Fed-friendly,” significantly boosting expectations for a potential rate cut by the Federal Reserve in September.

Fed Rate Cut Probabilities

Market predictions for Fed actions have shifted:

- July meeting: About 90% probability of no rate cut

- September meeting: Approximately 70% probability of a rate cut, up from a 50% chance just last week

The Week in Charts

What’s Going On In Your Portfolio?

Portfolios remain fully invested, favoring growth over value. Volatility stops remain in place in case of any unforseen events from either political or economic news.

Bond portfolios continue to be fully invested in High Yield bonds, which will benefit from the potential of lower rates in 2025.

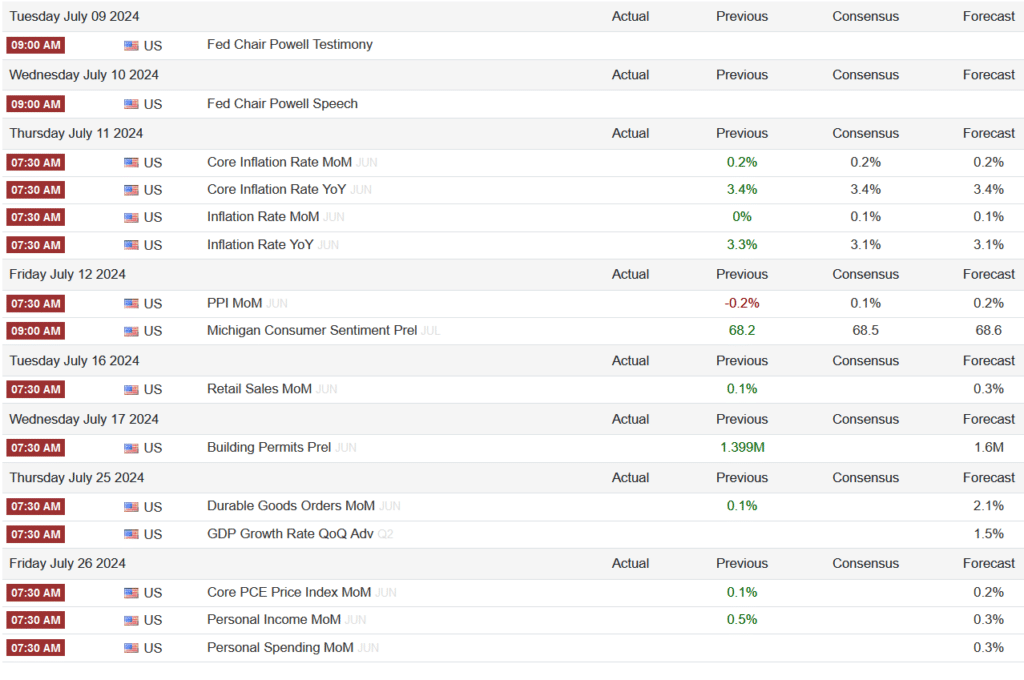

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics