Market Recap

In a condensed trading week of just four days, major U.S. stock indices managed to build on their monthly and quarterly advancements. The spotlight was on the Russell 2000, which surged 1.5%, significantly outperforming its larger and mid-sized counterparts, with value stocks beating growth stocks by nearly 2%.

Market activity was on the lighter side as investors were particularly cautious, awaiting the economic fallout from the Baltimore port closure. This incident severed shipping connections to one of the largest U.S. ports, critically affecting automobile and truck deliveries.

The Commerce Department revealed that orders for durable goods in February rose by 1.4%, surpassing expectations. When excluding the unpredictable defense and aircraft sectors, a measure more indicative of business investment climbed by 0.7%, also above forecasts.

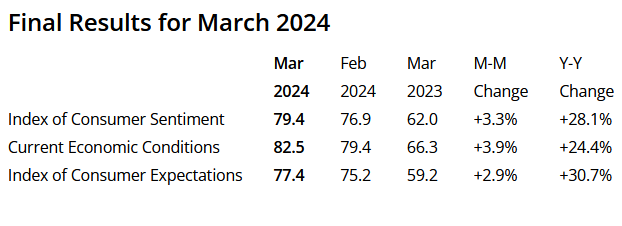

Meanwhile, new home sales unexpectedly dipped in February, revealing a mix in consumer sentiment; short-term optimism was tempered by longer-term concerns. On a positive note, the University of Michigan’s consumer sentiment index reached its highest point in 21 months on Thursday.

Source: University of Michigan

Weekly Chart Review

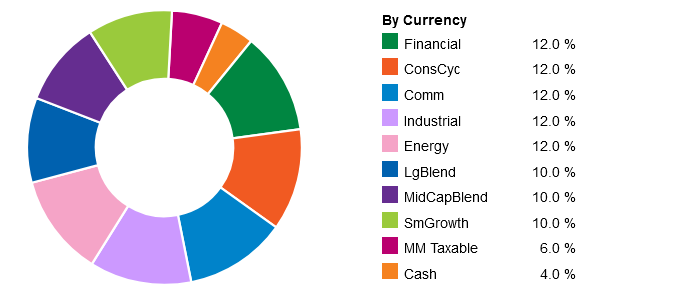

What’s Going On In Your Portfolio?

I have been shifting our client portfolios away from technology and into more value-oriented sectors. As inflation remains “sticky” the outlook for interest rate cuts continues to diminish.

At the start of 2024, the market was predicting 5-6 rate cuts. However, the probability of 1 or potentially 0 rate cuts is increasing.

This change in outlook has been benefiting the US dollar. Unfortunately, a stronger dollar could mean weaker technology stocks – similar to what occurred in 2022.

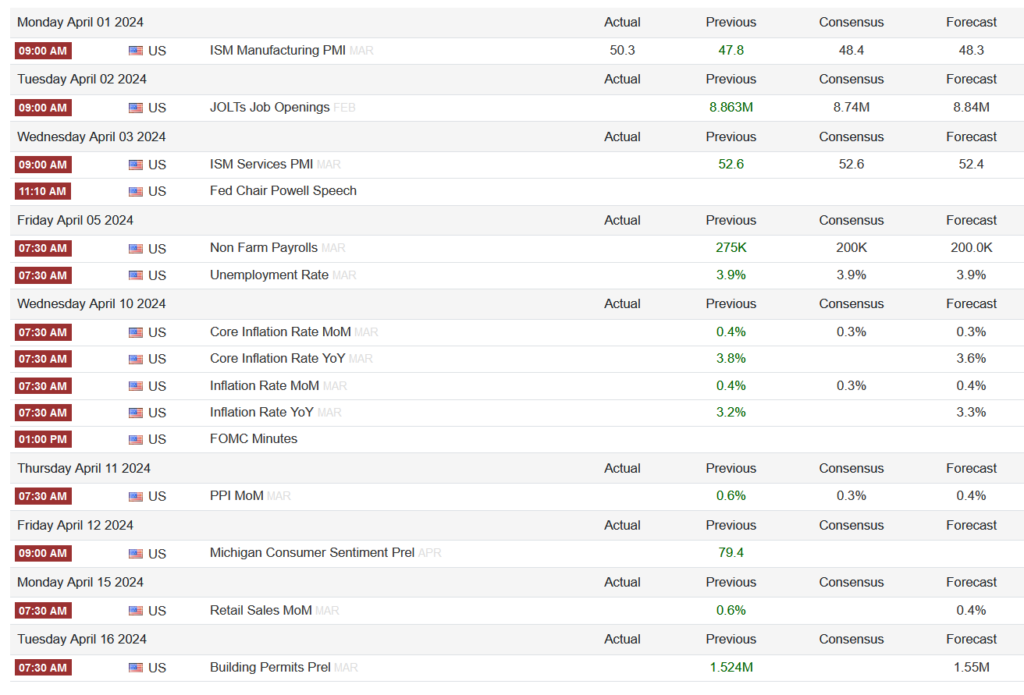

Upcoming Economic Data to Keep an Eye On

Looking Ahead Source: Trading Economics

Source: Trading Economics