The Week in Charts

Market Recap

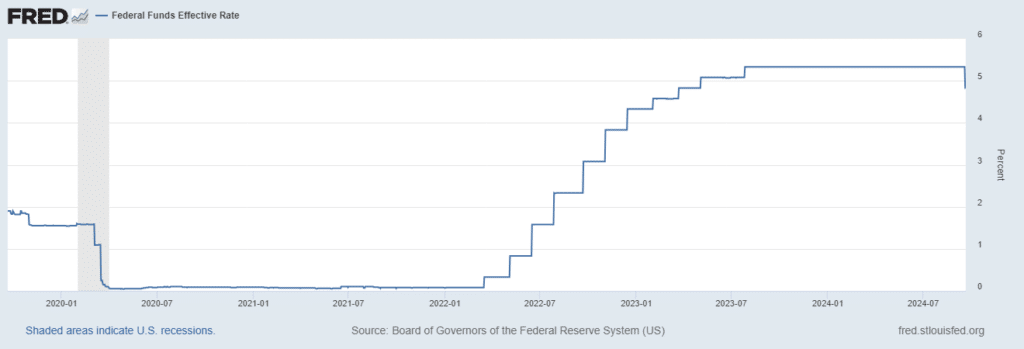

U.S. Stocks Continue to Climb Amid Fed Rate Cut

U.S. equities enjoyed another week of solid gains, building on the previous week’s impressive performance. The primary driver behind this upward momentum was the Federal Reserve’s unexpected decision to cut the federal funds rate by 50 basis points. While the size of the rate cut surprised some, the real cause for celebration on Wall Street was the indication that this move marks the beginning of a new rate-cutting cycle by the Fed.

Initially, markets pulled back following the Fed’s announcement. However, heavy trading volume and positive performance over the next two days propelled the DJIA, S&P 500, and NASDAQ to new highs. Although the smaller-cap Russell 2000 also saw gains, it remains about 9% below its record high from November 2021.

Economic Data Highlights

This week was rich in economic data, most of which was positive, leading some to question whether the Fed’s 50 basis point rate cut was too aggressive compared to a more modest 25 basis point cut.

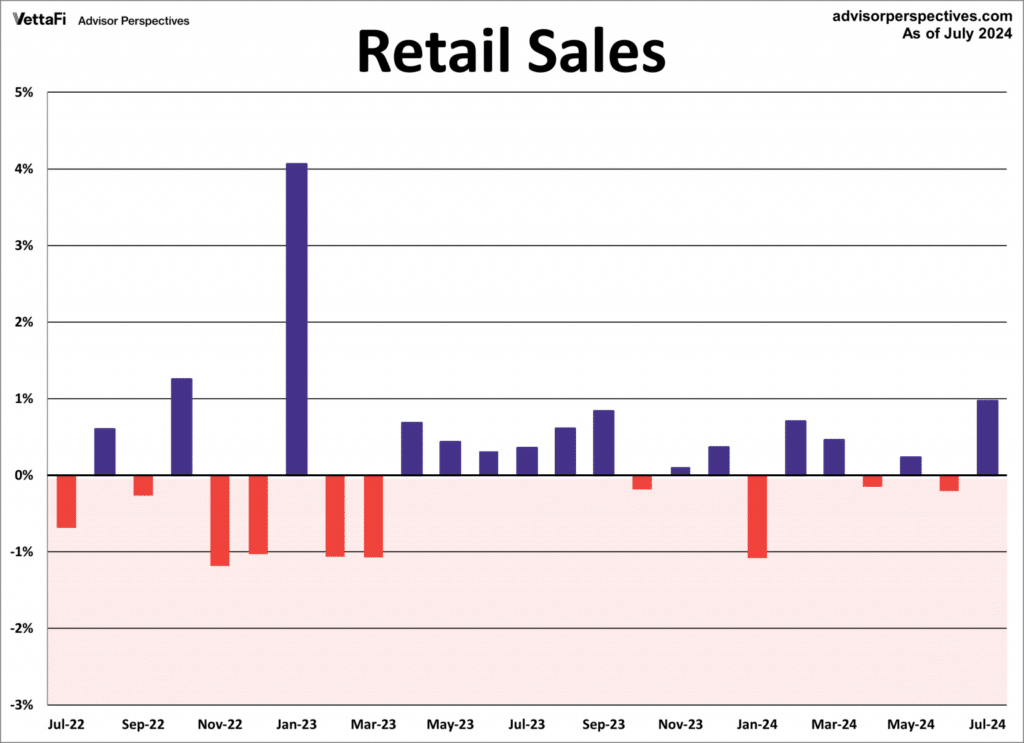

On Tuesday, the Commerce Department reported a 0.1% rise in Retail Sales for August, exceeding expectations.

The real surprise, however, was the upward revision of July’s Retail Sales to 1.1%. Additionally, continuing jobless claims fell to their lowest level in three months, as reported on Thursday.

Housing Market Developments

The Fed’s rate cut is expected to provide a boost to the stalled housing market. On Wednesday, the Commerce Department announced that building permits rose by 4.9% in August, marking their largest monthly gain in a year.

However, the National Association of Home Builders reported the next day that sales of existing homes fell by 2.5% in August. Interestingly, Fed Chair Jerome Powell emphasized in his Wednesday press conference that the central bank has limited influence over the housing market in general.

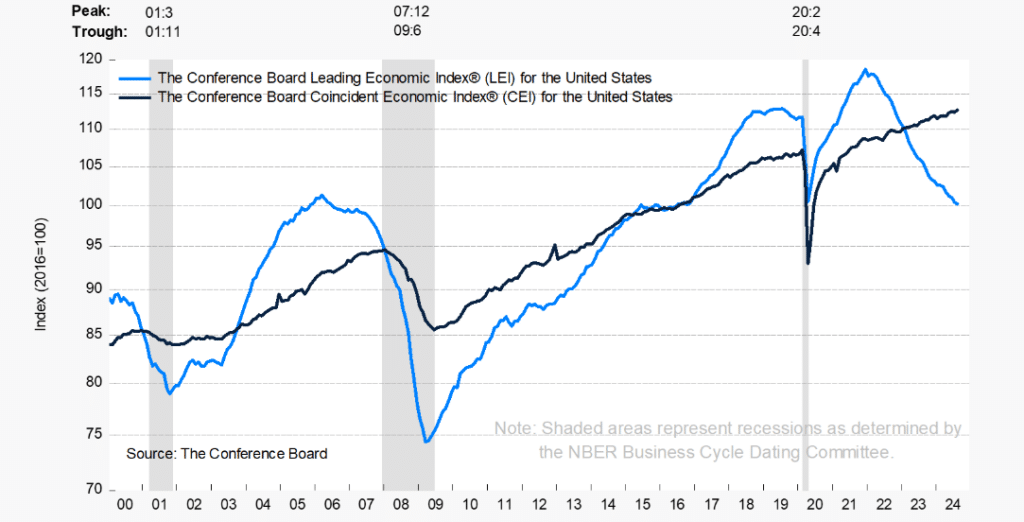

Leading Economic Index

The Conference Board Leading Economic Index (LEI) for the U.S. declined by 0.2% in August 2024 to 100.2, following an unrevised 0.6% decline in July. Although the LEI has been falling throughout 2024, the rate of decline has slowed compared to the previous year.

Between February and August 2024, the LEI decreased by 2.3%, a smaller drop than the 2.7% decline observed between August 2023 and February 2024.

Builder Sentiment Improves

Builder confidence in the market for newly built single-family homes rose in September, according to the National Association of Home Builders/Wells Fargo Housing Market Index. The index increased to 41, up from 39 in August, breaking a four-month streak of declines. All three HMI indices saw gains in September:

- Current sales conditions rose by one point to 45.

- Sales expectations for the next six months increased by four points to 53.

- Traffic of prospective buyers posted a two-point gain to 27.

The survey also revealed that the percentage of builders cutting prices dropped for the first time since April, down one point to 32%. The average price reduction was 5%, the lowest since July 2022. Additionally, the use of sales incentives fell to 61% in September, down from 64% in August.

What’s Going On In Your Portfolio?

I have been taking some profits from our value holdings and reallocating towards growth as opportunities present themselves. Volatility stops are still in place in case of a spike in volatility before the US Presidential election.

I have been taking some profits from our value holdings and reallocating towards growth as opportunities present themselves. Volatility stops are still in place in case of a spike in volatility before the US Presidential election.

Bond portfolios continue to be fully invested in High Yield bonds, which is an indication that the longer-term trend of the market is still intact.

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics