The Week in Charts

Market Recap

The first two weeks of 2025 have proven difficult for U.S. equities, with all major indices experiencing declines. Markets were closed on Thursday to honor the late President Jimmy Carter, contributing to a shortened trading week.

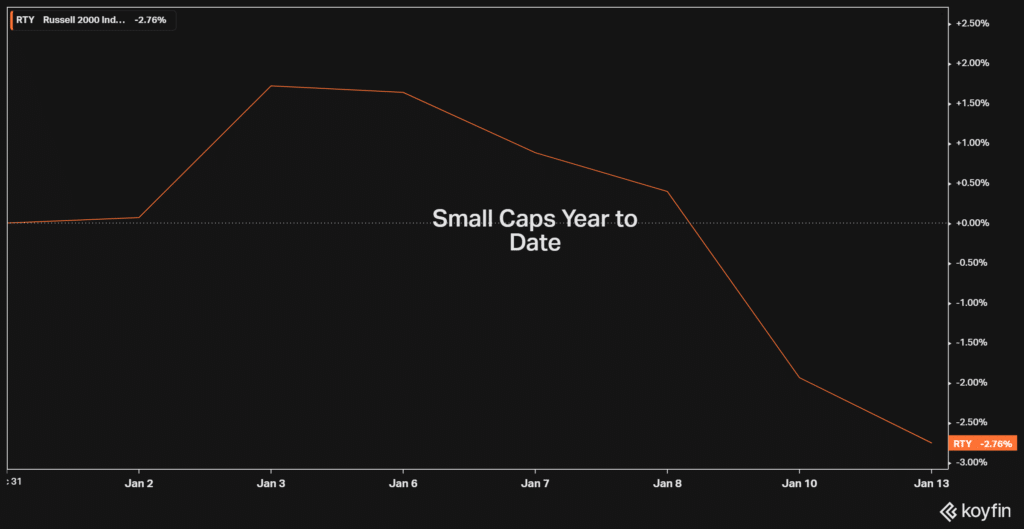

Small-cap stocks continued to struggle, with the Russell 2000 Index entering correction territory after underperforming large-caps for the fifth time in six weeks. Value stocks outperformed growth, while the NASDAQ suffered its most significant weekly loss since November 2024.

Friday’s trading was particularly challenging, as a surprisingly strong jobs report intensified concerns about potential delays in Federal Reserve interest rate cuts.

The Dow Jones Industrial Average, S&P 500, and NASDAQ each fell 1.6%, with Information Technology, Financials, and Real Estate sectors experiencing losses exceeding 2%.

Inflation and Interest Rate Concerns

Investors remain worried about persistent inflation and its impact on Federal Reserve policy. Federal Reserve Governor Michelle Bowman’s recent speech highlighted that inflation remains “uncomfortably above” the Fed’s 2% target, despite progress made in 2023. Minutes from the December Fed meeting revealed widespread concern among participants about potential upside risks to inflation.

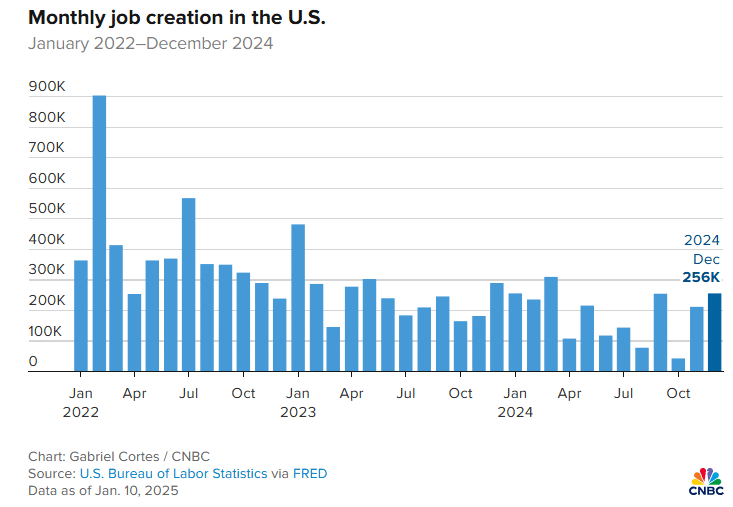

The Labor Department’s December jobs report, released on Friday, showed unexpectedly strong job growth of 256,000, surpassing forecasts. The unemployment rate dropped to 4.1%, below the anticipated 4.2%, further fueling speculation about delayed interest rate cuts.

Consumer Sentiment and Inflation Expectations

January’s consumer sentiment remained relatively stable, with only a slight decrease from December. While assessments of personal finances improved, short-term and long-term economic outlooks deteriorated.

Notably, inflation expectations for both the short and long term increased significantly:

- Short-term (year-ahead) inflation expectations rose from 2.8% to 3.3%, the highest since May 2024.

- Long-term inflation expectations increased from 3.0% to 3.3%, marking a rare large one-month change.

These increases were observed across various demographic groups, with lower-income consumers and political independents showing particularly strong shifts. While inflation uncertainty has risen over the past year, it remains below levels seen in the 1970s.

This situation presents a complex economic landscape as we move further into 2025, with strong job growth potentially delaying anticipated interest rate cuts and rising inflation expectations adding to market uncertainty.

What’s Going On In Your Portfolio?

Client portfolios remain in cash and/or hedged, as the major US indices remain in an intermediate downtrend.

Client portfolios remain in cash and/or hedged, as the major US indices remain in an intermediate downtrend.

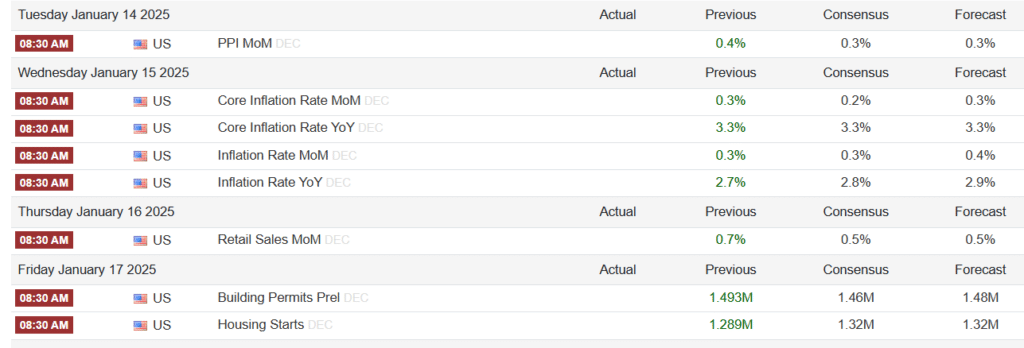

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics