Market Recap

U.S. equity markets experienced another volatile week with mixed performance across different market segments. The Dow Jones Industrial Average (DJIA) and Russell 2000 outperformed, while the S&P 500 and NASDAQ struggled:

- DJIA: +0.7% (40,589)

- S&P 500: -0.8% (5,459)

- NASDAQ: -2.1% (17,358)

- Russell 2000: +2.7% (2,260)

Key Highlights:

- Sector Performance: Communication Services, Information Technology, and Consumer Discretionary sectors underperformed, while defensive sectors like Materials and Utilities outperformed.

- Earnings: Major tech companies like Google (Alphabet) and Tesla released earnings, but failed to impress investors, contributing to the tech sector’s weakness.

- Economic Data:

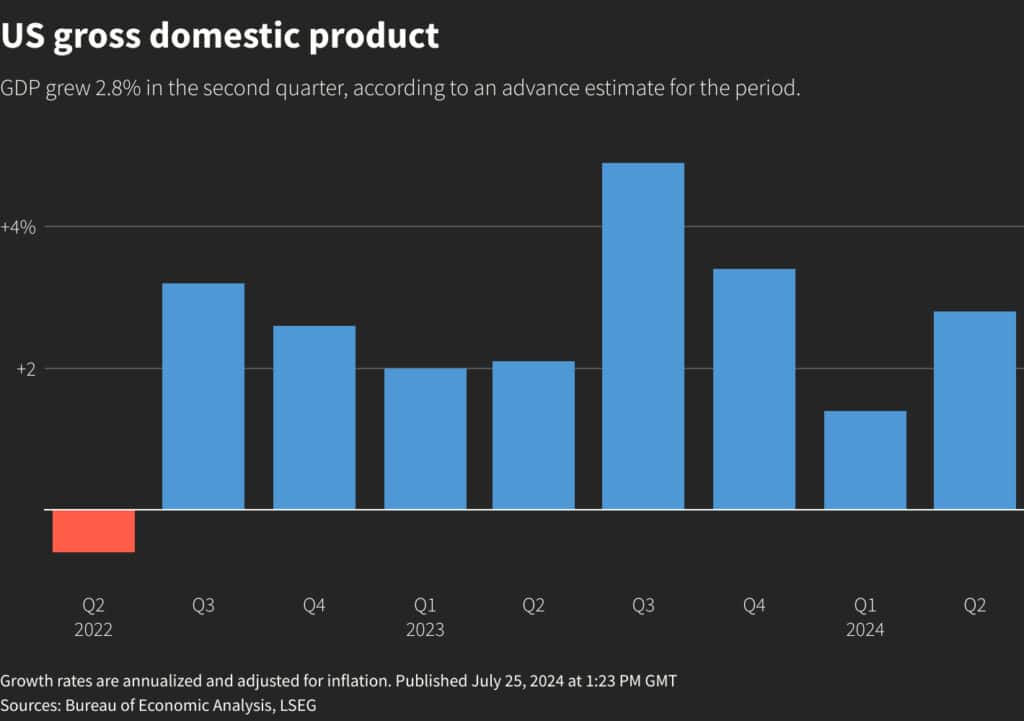

- Q2 GDP growth doubled from Q1, reaching 2.8%.

- Existing home sales dropped 5.4%, while average prices hit a new record high.

- Durable goods orders fell 6.6% in June, the sharpest drop since the pandemic.

- Initial jobless claims decreased to 235,000, lower than expected.

- Consumer sentiment slightly declined to 66.4 in July.

- Q2 GDP growth doubled from Q1, reaching 2.8%.

- Market Sentiment: The VIX (the market’s fear index) increased by 2% following last week’s 27% jump.

- Oil Market: WTI Crude oil prices declined 3.4% to $76.44 per barrel.

- Federal Reserve Expectations: Market participants are increasingly betting on a potential rate cut in September.

Notable Trends:

- Small-cap stocks continued to outperform for the third consecutive week.

- Value stocks outperformed growth stocks.

- The housing market shows signs of cooling, potentially shifting from a seller’s market to a buyer’s market.

Overall, the week’s economic data and market performance suggest a complex and confusing economic landscape, with investors closely watching for signs of potential changes in Federal Reserve policy.

The Week in Charts

What’s Going On In Your Portfolio?

Client portfolio’s have been raising cash as the increased volatility caused numerous sells signals to be triggered.

The current “state of confusion” within the market caused by President Biden’s annoucement that he will not seek relection, plus stronger than expected GDP numbers, have investors raising cash as they await this week’s FOMC meeting.

Bond portfolios continue to be fully invested in High Yield bonds, which is an indication that the longer term trend of the market is still intact.

I will be closely watching to see how the market react’s to the FOMC meeting, and any an opportunities that may arise.

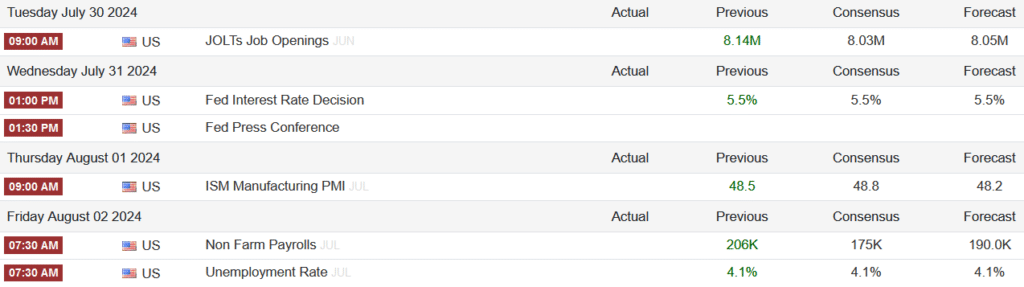

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics